・The main factor driving up raw material prices is the extreme imbalance between supply and demand. The global container shortage is likely to last until 2022.

・Raw material prices forecast to remain high for the reset of 2021.

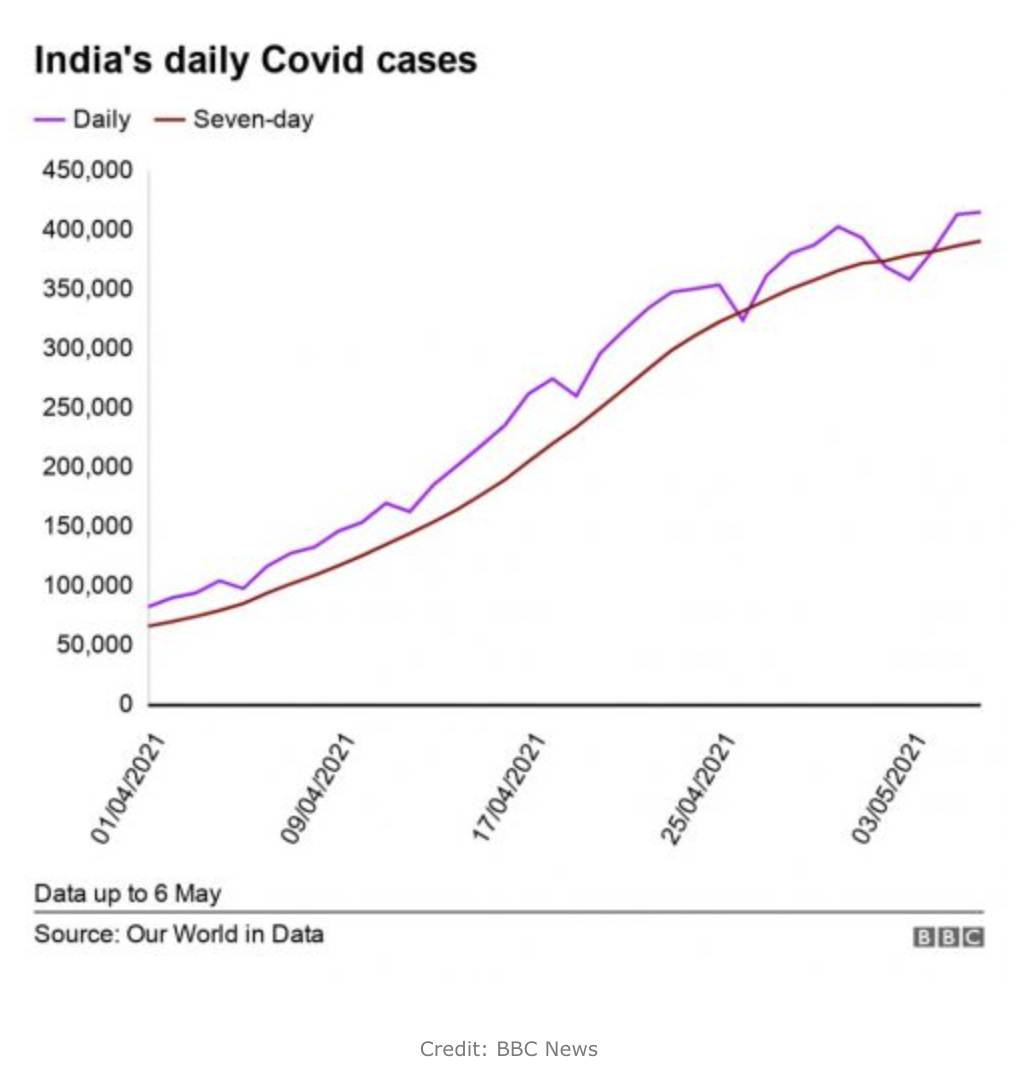

・While lockdown is being lifted across Europe, India is hit by serious second waves. This may cause delays in their infrastructure construction projects and have a further impact on global supply chain.

In May 2021, the copper price hits $10,000 per tonne for the first time in 10 years, and CME lumber futures price reached almost $1700 per mbf. Global pulp price has increased by 55% and seems to continue to rise. The oil price has risen by 70 percent, hitting $70 per barrel since November 2020. And so too are plastics, the U.S. export prices of PVC have nearly doubled to a record high of $1,775 per tonne over the past year and the prices of other plastics materials also increased by 20% to 50%.

The satellite captured this view of the Ever Given container ship stuck in the Suez Canal. Credit: Satellite image ©2021 Maxar Technologies.

3.Unexpected natural disasters in Texas, USA – Plastics plants in Texas have to suspend production due to the recent winter storm which caused up to 85% of U.S. production capacity of 3 of the most widely used plastic polymers in the world (PE, PP and PVC) has temporarily been disrupted.

256 bit SSL Encryption

256 bit SSL Encryption